One of the key reasons business owners buy insurance is to make sure they’re covered or protected if something goes wrong.

This is where the claims process comes in – having a claim accepted and paid by your insurer can help you to recoup costs and limit interruptions.

When you make a business insurance claim, it’s likely to be during a stressful period. That’s why being prepared and understanding how claims work improves the chances of a smooth process.

Recap – how do claims work?

You may need to make a claim if something goes wrong at your business. This could be something like a burst pipe causing flooding or theft of your business equipment.

To make a claim, you’ll need to notify your insurer (or their claims handler) to explain what’s happened. They’ll usually ask you for supporting evidence (such as photos and receipts) and then assess your claim against your insurance policy.

During this time, they’ll work out if you’re covered for what you’re claiming for, how much you could be paid, and any deductions from your claim (such as excess).

Depending on the nature of your claim, your insurer may send someone out to assess the issue (known as a loss adjuster).

If your claim is accepted, you’ll receive a settlement.

How long does a business insurance claim take?

Depending on the nature of your claim, it could take weeks or months.

A claim could take longer if there’s a lack of evidence or it’s a complex issue that requires a loss adjuster.

That’s why it’s so important to have all the right information and understand the claims process before you get started.

Helping businesses to get back on track

At Simply Business, our specialist claims partner1 paid out £128,000 a day in claims on average in 2025, helping our customers get back to business.

They paid out over £54 million in claims in 2025, with over 95 per cent of our settled claims paid in 24 hours (from the point of settlement)2.

Promotion

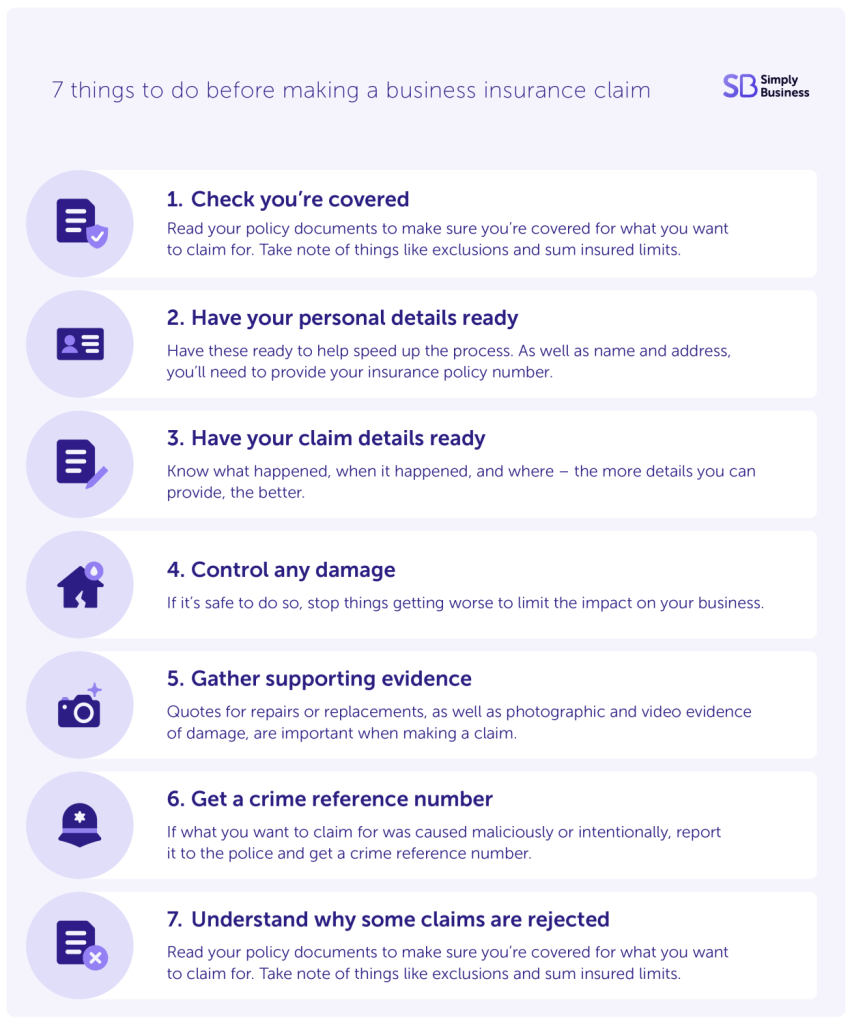

7 things to do before making a business insurance claim

If you think you might need to make a claim on your business insurance, follow these steps to help give yourself the best chance of a smooth and successful experience.

1. Check what you’re covered for

Before you make a claim, read your policy documents first. This can help you to confirm that you’re covered for what you want to claim for. You can also find your excess on your policy documents – the amount you need to pay towards your insurance claim.

It’s also worth checking:

- sum insured limits – the maximum amount of money your insurer will pay out for a claim

- exclusions – anything that isn’t covered by your insurance policy

If you don’t understand your policy documents, you should contact your insurer for help.

2. Have your personal details ready

When you submit a claim, the first thing you’ll be asked for is your personal details. Having these ready to go can save time and get the claims process started.

Details you’ll need to provide usually include:

- full name

- address

- policy number

3. Have your claim details ready

As well as personal details, your insurer will want to know about what you want to claim for. Be ready to explain what happened and when.

Specifically, it could be useful to note down the following:

- date and time – when the incident happened (or when you first discovered it)

- location – be as specific as possible, for example where at your premises did an incident take place

- event details – give as many facts as you can about what happened to help your insurer build a picture of the situation

4. Damage control

If something is damaged or broken and you need to make a claim, do what you can to control the situation. It’s important to note that you should only do this if it’s safe to do so without any further risk. If you’re able to limit damage, you could stop things getting worse. As a result, getting your claim accepted and settled could be quicker and easier.

On top of this, the more you limit any damage, the less disruption it could cause to your business.

5. Gather supporting evidence

Providing evidence is a crucial part of the claims process. The more useful evidence you can provide, the higher your chances of a quick and successful insurance claim.

Here are some of the things that could help your claim:

- repair quotes or receipts – provide several estimates for repairs or replacements to damage. Or if you’ve got the work done already, provide the receipts

- inventory – a list of the items or damage you want to claim for. Give as many details as possible, such as purchase price, ages, makes, models, etc.

- photographs and videos – clear visuals of any damage can be vital in helping you to get the right result for your claim

6. Get a crime reference number

If the damage you want to claim for was caused maliciously or intentionally, you should report it to the police. They’ll give you a crime reference number, which you can then provide to your insurer when you report your claim.

7. Understand why claims are rejected

Not all claims reach a settlement, while others may not even be accepted. It’s important to understand why claims may be rejected so you can set realistic expectations. If you know what you want to claim for will be rejected, you don’t need to waste your time making a claim.

Here are three reasons why a claim could be rejected:

- Undisclosed information – you’ve withheld information that influences an insurer’s decision to cover you. For example, you have more employees than you stated when buying a policy.

- Missing information – your personal details have changed (such as your business address) but you didn’t let your insurer know.

- Violation of policy terms – you’ve broken the terms in your insurance policy. For example, your premises are broken into but weren’t secured in the way stated in your policy. Other exclusions include gradual deterioration of items over time (known as wear and tear) and items being left unsecured.

What happens after you’ve made a claim?

Firstly, the insurer will usually assign a claims handler to your case. They’ll review your policy to confirm if it covers what you’re claiming for. You’ll then be given a claim reference number.

If it’s a simple claim, the claims handler may be able to settle based on the evidence you provide. For more complex claims, you may be asked for more evidence or visited by a loss adjuster to investigate.

The next step is that the insurer (or their claims handler) will work out the value of the claim and offer you a settlement – an amount of money minus your excess. Alternatively, they may arrange for a contractor to carry out works, in which case you wouldn’t receive a cash settlement.

It’s important to note that the process is likely to be different depending on your insurer or claims handler.

More business insurance guides

- Why insurance claims get delayed (and how to avoid it)

- What is an insurance broker? (and other ways to buy business insurance)

- What is ghost broking? How to avoid insurance scams

- What is excess in insurance? A UK guide

- Sedgwick International UK (SIUK) manages insurance claims as a third-party administrator on behalf of various insurers, each of whom holds the necessary permissions from the Financial Conduct Authority (FCA). Further information about Sedgwick can be found on their website. ↩︎

- This figure is rounded across our range of products. “Settled” covers paid claims (and excludes declined or withdrawn claims). Our claims process may vary for different products and operates on a ‘claim by claim’ basis. Our specialist partner Sedgwick will pay the claims on behalf of the insurer. ↩︎