As a landlord, you must pay tax on the profit you make from renting out a property. Your rental income is taxed at the same rate as other employment, and you’ll need to declare this income to HMRC by completing an annual Self Assessment tax return.

Understanding your tax obligations is a crucial part of being a landlord. This guide explains everything you need to know about tax on rental income, including new rates on property income from 2027, allowable expenses, and how to file your tax return.

What taxes do UK landlords need to pay?

If you receive income that isn’t taxed at the source (through PAYE), you need to submit a Self Assessment tax return to HMRC. Landlords may need to pay several types of tax throughout their time renting out property.

Key landlord taxes include:

- National Insurance contributions (NICs)

- stamp duty land tax

- capital gains tax

- council tax

- inheritance tax

Not all of these are paid through Self Assessment. For example, you only need to pay stamp duty land tax and capital gains tax when buying or selling a property.

How much tax do you pay on rental income?

Your rental income is taxed at the same rate as income from employment. This income is added to any other earnings you have, which could push you into a higher tax bracket.

The income tax rates are:

- 0% on income up to £12,570 (personal allowance)

- 20% on income between £12,571 and £50,270

- 40% on income between £50,271 and £125,140

- 45 per cent on income above £125,140

It’s important to note that these rates will be increased by two per cent from April 2027 – find out more below.

For example, if you earn £15,000 a year from rental income plus £45,000 from a self-employed job, your total income is £60,000. You would pay:

- 0% on the first £12,570

- 20% on the next £37,700

- 40% on the final £9,730

You need to complete a landlord tax return by 31 January each year if you make a significant amount of money from renting out property.

Paying the right amount of tax can be tricky, so remember to speak to an accountant or professional tax adviser if you’re unsure of anything.

Landlord tax return example

In this example, the landlord receives £1,800 a month in rent from their tenant, leaving them with an annual rental income of £21,600.

Their allowable expenses (including letting agent fees and contents insurance) add up to £3,000, meaning their taxable rental income is £18,600.

The first £12,570 is taxed at 0% due to the personal allowance, and the next £6,030 is taxed at 20%.

This leaves a tax bill of £1,206. As the landlord pays £200 a month in buy-to-let mortgage interest, they can claim a 20% tax credit of £480.

This leaves a final bill to HMRC of £726.

If the landlord had other earnings, it would push up their tax bill significantly. Adding a £40,000 annual salary from a self-employed job to the above example would mean the landlord has to pay:

- 20% on £10,270 of rental income = £2,054

- 40% on £8,330 of rental income = £3,332

This would leave them with a final tax bill of £4,906 as their self-employed job pushes them into the higher tax band.

You can use a landlord tax calculator to work out how much your bill could be.

New tax rates on property income from 2027

Announced as part of the Autumn Budget 2025, new income tax rates for property income will be introduced from April 2027.

The new tax rates will be two per cent higher than standard income tax rates:

| Tax band | Standard income tax rate | New property income tax rate (from April 2027) |

| Basic rate (£12,570 – £50,270) | 20% | 22% |

| Higher rate (£50,271 – £125,140) | 40% | 42% |

| Additional rate (Over £125,140) | 45% | 47% |

Landlords will continue to pay normal income tax rates on their salary and other earnings. And property tax will still be paid on rental profits after allowable expenses have been deducted.

If you have a buy-to-let mortgage, the tax relief credit will be increased from 20% to 22%.

‘Risking a steady long-term rise in rents’

The new system addresses the fact that landlords don’t pay National Insurance, while most of their working tenants do.

However, a report published by the Office for Budget Responsibility (OBR) said costs for landlords will increase.

“This successive eroding of private landlord returns will likely reduce the supply of rental property over the longer run.

“This risks a steady long-term rise in rents if demand outstrips supply.”

Landlord tax relief – what is the rental income tax allowance?

You get a £1,000 tax-free rental income tax allowance each year, which you can claim on your tax return.

However, a landlord’s rental income will almost certainly be more than £1,000 a year, and you can’t claim any other expenses if you use the property allowance. This means the allowance is only useful if you have less than £1,000 in expenses from renting out your property.

Do landlords pay National Insurance on rental income?

You will need to pay Class 2 National Insurance if your profits are £6,725 a year or more and being a landlord is your main job. This generally applies if you’re running your rental operation as a business.

HMRC considers you to be running a property business if all these conditions apply:

- being a landlord is your main job

- you rent out more than one property

- you’re actively buying new properties to rent out

If you don’t meet these criteria, you don’t need to pay National Insurance on your rental income. However, you may be able to pay voluntary Class 3 National Insurance contributions instead.

How does corporation tax work for landlords?

Some landlords create a limited company to manage their properties. This means profits are subject to corporation tax at 19% or 25%, rather than personal income tax rates. While this can be more tax-efficient, running a limited company involves more administrative work and costs.

Read more: Record number of landlords open property companies

What happens if I make a loss on my rental property?

If your annual expenses are higher than your rental income, then you’ll make a loss and won’t be required to pay tax for that year.

This loss can be carried forward and deducted from any rental profits you make in future tax years.

For example, if you made a £2,000 loss in the 2025-26 tax year and a £3,500 profit the following year, you can offset the loss. This means you would only pay tax on £1,500 of profit.

What are the tax rules if you own multiple properties?

If you own several rental properties, you can combine the income and expenses to calculate a total taxable income. This can help to reduce your final tax bill.

It’s important to note that any income for overseas properties or furnished holiday lets should be kept separate.

How do I complete a landlord Self Assessment tax return?

The Self Assessment process for landlords is straightforward if you follow these six key steps.

Here are six simple steps to follow:

1. Register for Self Assessment

The first thing you need to do is register for Self Assessment.

You usually need to register by 5 October in the tax year after you begin receiving rental income. So, if you start receiving rental income in the 2026-27 tax year, you’ll need to register by 5 October 2027.

When you register, you should get a Government Gateway user ID and password. With this you can set up your personal tax account, which lets you manage your taxes online.

Once you’re registered, you can then file your tax return by filling out the Self Assessment tax return form either online or on paper (paper returns are gradually being phased out due to Making Tax Digital).

2. Know key tax deadlines

The deadline for submitting your tax return for each financial year is usually 31 October for paper tax returns and 31 January for online tax returns. So for the 2025-26 tax year, the deadline for paper tax returns is 31 October 2026 and the deadline for online tax returns is 31 January 2027.

Once you’ve filed your tax return, you then need to pay the tax you owe. The deadline is the same as the final date for online Self Assessment tax returns, so the deadline for paying your 2025-26 tax is 31 January 2027.

There are penalties for missing the deadlines, so don’t delay getting yours ready.

3. Gather the right information

To fill in your tax return you’ll need information about all the income you’ve received throughout the tax year, as well as information about expenses you want to deduct.

HMRC says you need to record:

- the dates you let out your property

- all the money you’ve spent (including cash, cheque, credit and debit card transactions)

- all rents received

HMRC lists the documents to keep in support of your records:

- lease or letting contracts

- rent books

- receipts

- invoices

- bank statements

- mileage logs (for journeys that are solely for your property business purposes)

- cost of the vehicle used for property business and its CO2 emissions

- for furnished holiday lettings and commercial premises, the costs of any other capital items used in the property

- all documents relating to when you bought the property

There’s accounting software available that can organise and keep track of your records for you.

You’ll also need your UTR (unique taxpayer reference) number, which is assigned to you when you register for Self Assessment.

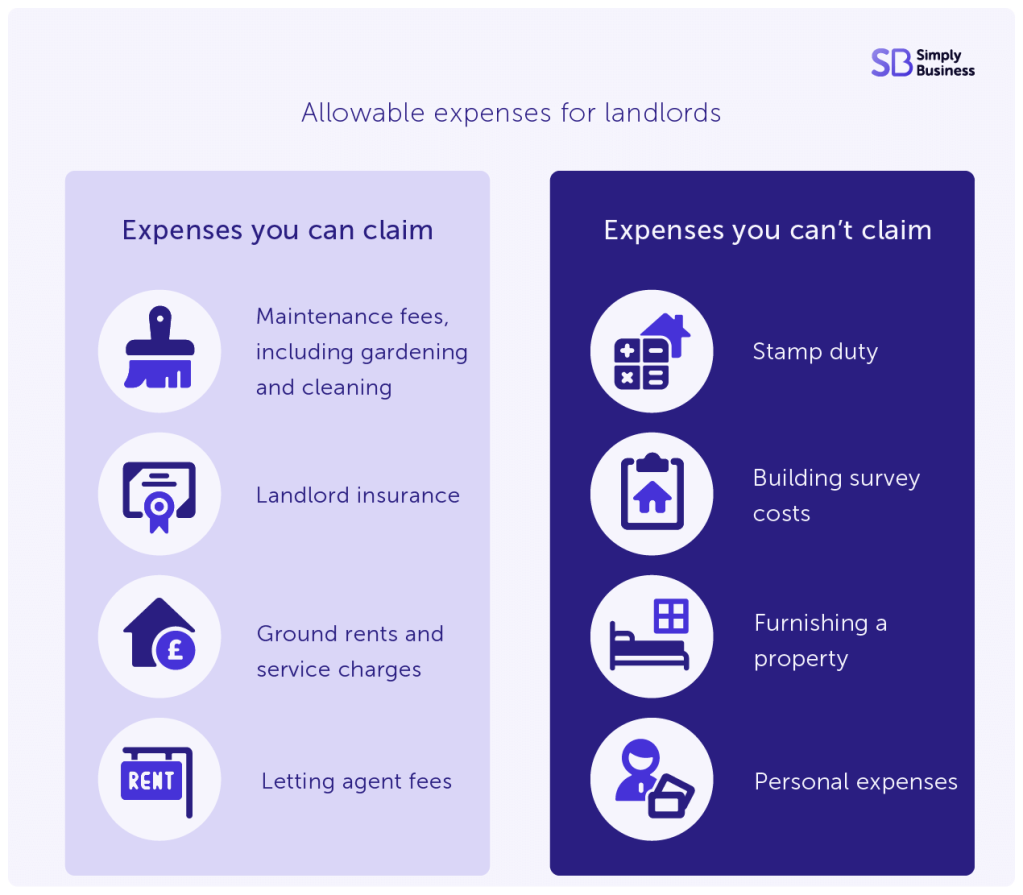

4. Calculate allowable expenses

There are a number of allowable expenses for landlords. You can use these landlord tax deductions to work out your total taxable profit. As a general rule, your expenses need to be ‘wholly and exclusively’ used for the purposes of renting out property.

Some of the main allowable expenses are:

- property repair and maintenance costs (but not improvements)

- accounting and letting agents’ fees

- landlord insurance

5. Fill in the landlord tax return

When you fill in your tax return online, HMRC’s system will ask you what type of income you receive, tailoring the return to your circumstances.

UK landlords will need to fill in the UK property section, where you’ll tell HMRC about:

- premiums from leasing UK land

- rental income and other receipts from UK land or property

- income from letting furnished rooms in your own home

- income from furnished holiday lettings in the UK or European Economic Area

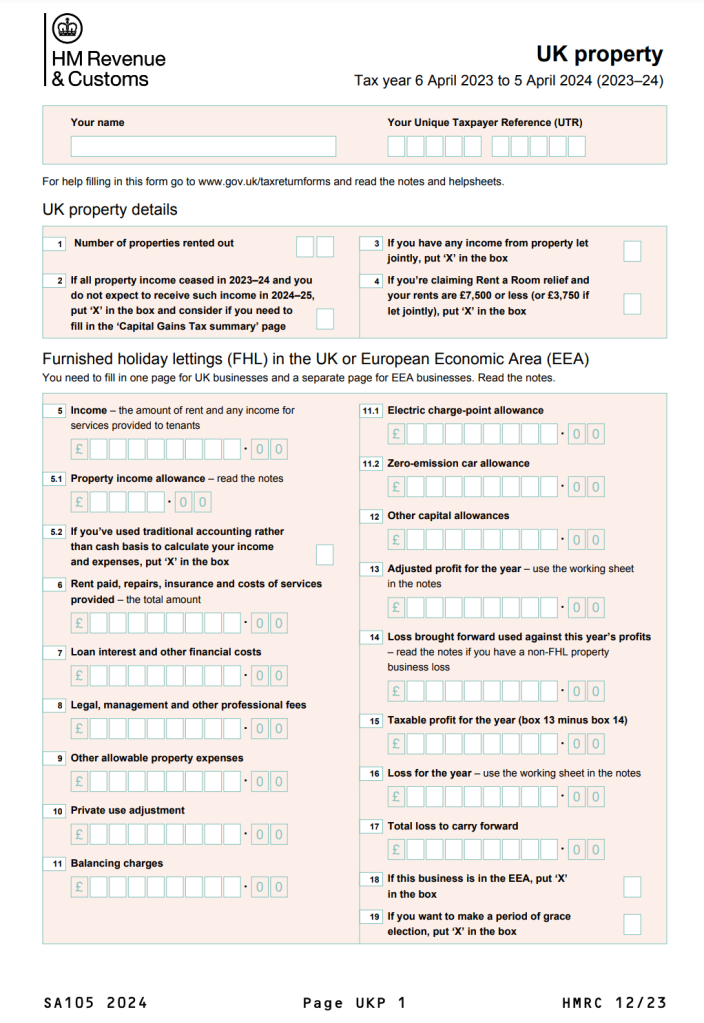

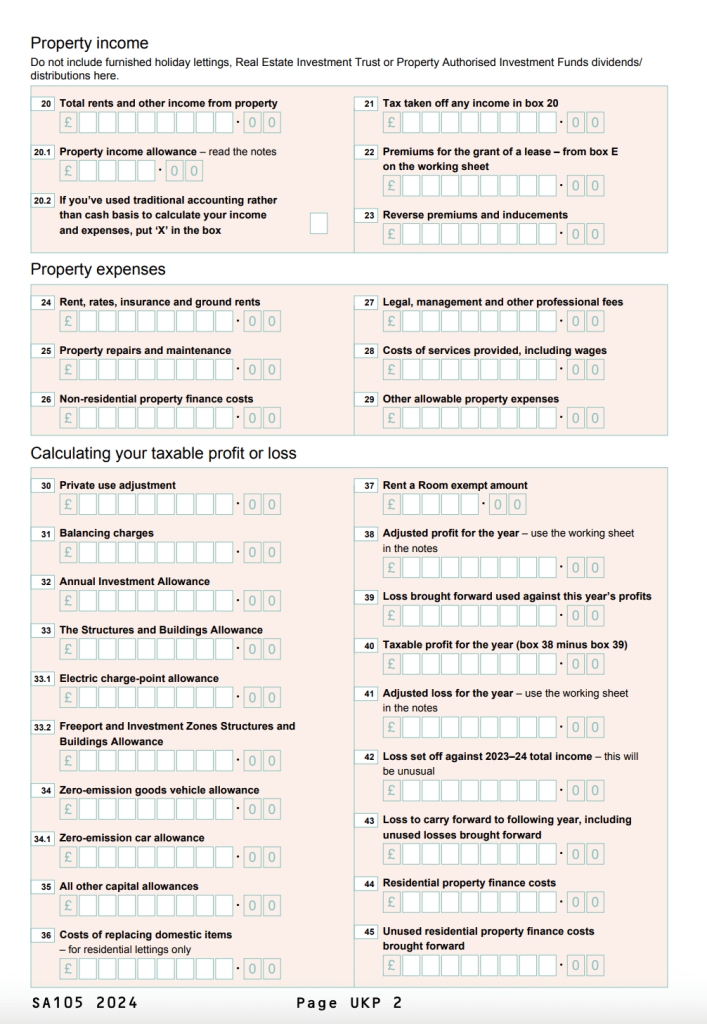

For paper tax returns, everybody needs to fill in form SA100.

Landlords should fill in the UK property supplement SA105 and any other relevant supplements (for example, SA103 if you’re also self-employed).

Pages one and of the SA105 form for filing your landlord tax return. Source: HMRC

6. Pay your landlord tax bill

HMRC will calculate what you owe and send you a tax bill. If you file online, you can see how much you owe under ‘View your calculation’.

If you send a paper return, you’ll get a bill in the post.

You’ll need your payment reference to pay your bill, which is your Unique Taxpayer Reference (UTR) number followed by the letter ‘K’.

The fastest ways to pay your tax bill are:

- online or telephone banking

- Chaps (Clearing House Automated Payment System)

- debit or corporate credit card online (you can’t pay using a personal credit card)

- at your bank or building society

You can also pay by Bacs, cheque, or Direct Debit, but these take longer.

If your bill is over £1,000, you’ll also need to make a payment on account, which is an advance payment towards your next Self Assessment bill.

If your bill is less than £30,000 for your payment due on 31 January 2027 and you think you’ll struggle to pay, you can use HMRC’s Time to Pay service to set up a payment plan.

What does Making Tax Digital mean for landlord tax?

Making Tax Digital (MTD) is a government initiative designed to make it easier for people to manage their tax affairs.

However, research from Simply Business shows that 68 per cent of landlords don’t feel prepared for Making Tax Digital.

- 41% think it will make tax returns more expensive (due to increased accountancy costs)

- 45% think it will make tax returns more time-consuming (due to quarterly submissions)

- 35% think it will make tax returns more complicated

For landlords, MTD for Income Tax Self Assessment (ITSA) will replace the current system. Instead of filing one annual tax return, you’ll send quarterly updates to HMRC about your income and expenses. At the end of the tax year, you’ll submit a final declaration to confirm your figures.

This new process is being introduced in stages. As of April 2026, landlords with an annual income over £50,000 will need to comply with MTD rules. It will then apply to those earning over £30,000 from April 2027 and those earning over £20,000 from April 2028.

To get ready, you should:

- keep digital records – all your business records, including rental income and expenses, must be stored digitally

- use compatible software – you’ll need to use software that’s compatible with HMRC’s systems to send your quarterly updates and final declaration

Landlord tax – 5 key takeaways

- Self Assessment is mandatory – you must declare your rental income to HMRC by completing a Self Assessment tax return each year.

- Rental income is taxed like other earnings – the profit from your rental property is added to your other income, which could move you into a higher tax bracket.

- You can deduct allowable expenses – costs that are ‘wholly and exclusively’ for renting out your property can be deducted to lower your taxable profit.

- Keep detailed records – to complete your tax return accurately, it’s essential to keep organised records of all income and expenses, including receipts, bank statements, and invoices.

- Know the key deadlines – you must register for Self Assessment by 5 October after the tax year you start earning rent. The online filing and payment deadline is 31 January.

Tax on rental income FAQs

What is the deadline for paying tax on rental income?

The deadline for paying your Self Assessment tax bill is 31 January each year. This is for the tax year that ended on the previous 5 April.

Can I deduct mortgage interest from my rental income?

You can no longer deduct mortgage interest directly from your rental income. Instead, you can claim a tax credit equivalent to 20% of your mortgage interest payments to reduce your final tax bill.

What happens if I live abroad?

If you live abroad for more than six months a year, you are a ‘non-resident landlord‘. You can either have tax deducted from your rent by your letting agent or tenant, or you can apply to pay tax through Self Assessment by completing form NRL1i.

What are new tax rates for property income?

From April 2027, the government will introduce separate tax rates for property income. This means landlords will pay higher tax on their rental profits.

The new rates will be:

- basic rate: 22% (currently 20%)

- higher rate: 42% (currently 40%)

- additional rate: 47% (currently 45%)

Get set with tailored landlord cover

Over 200,000 UK landlord policies, a 9/10 customer rating and claims handled by an award-winning team. Looking to switch or start a new policy? Run a quick landlord insurance quote today.